₹1,196 Crore Fake GST ITC Case: DGGI Investigation Ka Ab Kya Status Hai?

The ₹1,196 crore fake GST ITC case was originally reported in February 2025 after the Directorate General of GST Intelligence, or DGGI, announced action against an alleged network of bogus companies, fake invoices and e-way bills. The matter attracted attention because of the large value of Input Tax Credit reportedly generated and passed through entities that allegedly had no genuine business operations.

ABR NEWS is publishing this follow-up report on July 18, 2026, to seek clarity about the present position of the investigation. At the time of publication, ABR NEWS had not independently verified any final recovery order, prosecution result, conviction, closure report or adjudication order connected with the case.

₹1,196 Crore Fake GST ITC Case: Background

According to the official information available at the time of the original report, the DGGI Pune Zonal Unit conducted searches at multiple locations in Pune, Delhi, Noida and Muzaffarnagar. Investigators alleged that a network of entities had been created or used for generating invoices without actual supply of goods.

The accused persons were alleged to have generated fake tax invoices and e-way bills for transactions that did not correspond with genuine commercial activity. Authorities reportedly examined RFID movement information connected with the e-way bills and found an absence of corresponding movement records in certain cases.

This alleged mismatch was treated as an indication that goods may not have physically moved as declared. The network was accused of facilitating the wrongful availment and passing of Input Tax Credit amounting to approximately ₹1,196 crore.

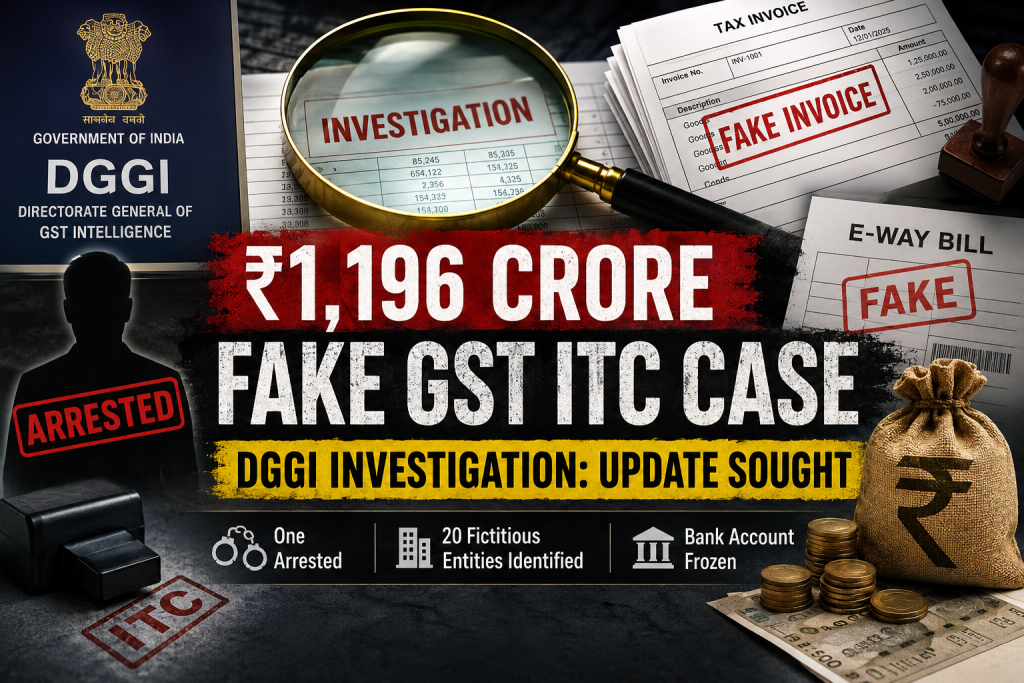

What DGGI Originally Reported in the GST ITC Investigation

- Fraudulent Input Tax Credit transactions of approximately ₹1,196 crore were allegedly detected.

- Searches were conducted in Pune, Delhi, Noida and Muzaffarnagar.

- One individual was reportedly arrested.

- Twenty allegedly fictitious entities were identified.

- One bank account connected with an allegedly fraudulent entity was frozen.

- Invoices, financial records, company stamps and seals were reportedly recovered.

- Personal identity details were allegedly used to obtain GST registrations.

The person arrested in the case was reported to be a director of a private company based in Muzaffarnagar. Authorities alleged that the individual played a central role in managing the entities and documents used in the suspected invoice network.

Investigators also reportedly recovered a database containing addresses, identity information, email addresses and mobile numbers. These details were allegedly rotated or reused for obtaining new GST registrations and avoiding detection.

₹1,196 Crore Fake GST ITC Case: Current Status Sought

More than a year after the original enforcement action, several important questions remain relevant for businesses, taxpayers and the public. ABR NEWS has sought an official update from the competent GST and DGGI authorities regarding the current status of the ₹1,196 crore fake GST ITC case.

The requested update includes information about the progress of the investigation, the amount of tax credit blocked or reversed, any recovery made, the status of the accused, action against beneficiary entities and whether prosecution or adjudication proceedings have been initiated.

Until a response is received from the relevant authority, it would be incorrect to claim that the entire alleged amount has been recovered or that all persons connected with the case have been prosecuted. Investigation, tax adjudication and criminal prosecution are separate legal processes and may proceed on different timelines.

How Fake GST Input Tax Credit Fraud Generally Works

Under the Goods and Services Tax framework, a registered business may claim Input Tax Credit for eligible GST paid on genuine business purchases. The credit can be adjusted against the GST payable on the business’s outward supplies, subject to statutory conditions and documentary evidence.

In a fake ITC arrangement, an invoice may be issued without any actual supply of goods or services. The recipient may then use that invoice to claim tax credit and reduce its GST liability. In more complex networks, several shell entities may circulate invoices through multiple layers to make the transactions appear genuine.

Fraudulent operators may use borrowed or misused identity documents, temporary addresses, multiple mobile numbers and bank accounts to obtain GST registrations. They may also create e-way bills even when no goods are transported.

Tax authorities increasingly compare GST returns, e-invoice data, e-way bills, bank transactions, transport records, vehicle information and RFID movement data. A significant mismatch between declared purchases and actual logistics activity can trigger investigation.

The ₹1,196 crore fake GST ITC case is important because it illustrates how invoice data, physical movement records and registration information can be examined together to identify suspected tax-credit networks.

Questions ABR NEWS Has Raised With GST Authorities

ABR NEWS is seeking clarification on the following points connected with the investigation:

- What is the present investigation status of the ₹1,196 crore fake GST ITC case?

- How much alleged Input Tax Credit has been blocked, reversed or recovered?

- Have any additional arrests, searches or summons been issued?

- Has a prosecution complaint, chargesheet or complaint before the competent court been filed?

- What action was taken against the 20 allegedly fictitious entities?

- Were their GST registrations suspended or cancelled?

- Were beneficiary companies or recipients of the alleged credit identified?

- What is the present status of the frozen bank account and any attached assets?

- Is any adjudication, appellate or court proceeding currently pending?

- Has any part of the investigation been completed or formally closed?

The official response, when received, should help establish whether the investigation has resulted in tax recovery, prosecution, additional enforcement action or any final legal determination.

ABR NEWS Analysis: Why the GST ITC Case Matters

The ₹1,196 crore fake GST ITC case highlights the compliance risks faced not only by alleged invoice operators but also by businesses purchasing from questionable suppliers. A buyer may face scrutiny when its supplier is found to be non-existent, inactive or unable to establish actual delivery of goods or services.

Businesses should therefore verify the GST registration status of vendors, maintain purchase orders, invoices, e-way bills, proof of delivery, transport records, payment trails and correspondence. Merely possessing an invoice may not be sufficient when the underlying supply cannot be demonstrated.

Companies should also monitor whether suppliers file their GST returns and whether invoice information appears correctly in the recipient’s available tax-credit records. High-value transactions with newly created or unfamiliar entities require stronger due diligence.

The use of RFID and logistics information in the original investigation also indicates that tax enforcement is becoming increasingly data-driven. Transactions declared on paper can be compared with vehicle movement, banking records and return filings to identify inconsistencies.

Frequently Asked Questions

It concerns an alleged network detected by DGGI in which fake invoices, e-way bills and allegedly fictitious entities were reportedly used to generate or pass fraudulent Input Tax Credit worth approximately ₹1,196 crore.

ABR NEWS has not independently verified any official confirmation that the entire alleged amount has been recovered. An updated response has been sought from the relevant authorities.

The original February 2025 report stated that one individual had been arrested. The present bail, prosecution or court status requires an updated official confirmation.

RFID and transport records may help establish whether goods linked with an e-way bill physically moved. The absence of corresponding movement can become a factor in examining whether the declared supply was genuine.

Official Sources and Related Coverage

For official information regarding GST intelligence and enforcement, visit the Directorate General of GST Intelligence and the Central Board of Indirect Taxes and Customs .